Introducing a 10-part Series on the Disruption of Capital Markets

Most Heritage Financial Firms will be Irrelevant by 2030

The above claim is not mine – it is the outcome of the recent 2018 CEO survey by Gartner (world’s leading research and advisory company). By 2030, 80 percent of heritage financial services firms will go out of business, become commoditized or exist only formally, struggling to compete with global digital platforms and Fintech (financial technology) startups. Therefore, it is no surprise that many major global financial firms are investing unfathomable amounts to stay competitive.

This article marks the fifth installment of the series, “Capital Markets: Past, Present, and Future”. While we have slowly unraveled the web of complexities inherent in capital markets, and the reasons for technological stagnation, inefficiencies start to become clear. And when you put these inefficiencies against the backdrop of today’s technologies, it really stresses the urgency to evolve.

“Software is eating the world” — Andreesen Horowitz

Andreesen Horowitz’s famous investment thesis above has unfolded under our very eyes and day-to-day lives, and capital markets are no exception to this rule. So let’s dive deeper into the tools at our disposal to drive the future’s tectonic shifts in the sector…

This deliberation is endless and admittedly one of my favorite topics; therefore for the sake of clarity and brevity, this article will remain at a high level. Below is a plethora of key technologies, capabilities, and trends currently impacting the capital markets’ evolution. The implications are myriad; some obvious, while others esoteric. For the discerned reader looking for more, the included references are a good starting point for each topic.

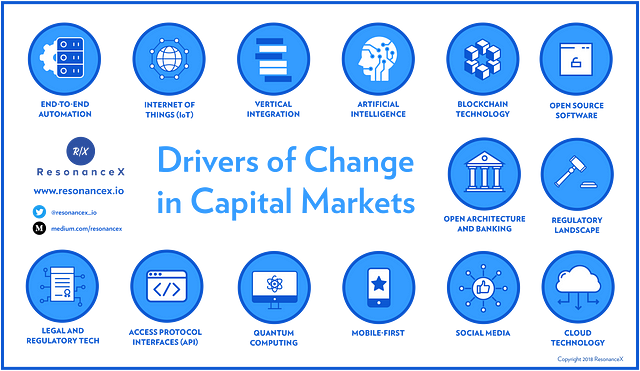

Drivers of change

End-to-End Automation

Automating all processes in a streamlined workflow without unnecessary interference by people, significantly reduces operational costs, risks, and headaches. Automation not only vastly speeds up customer experience (e.g. the potential customer-churning client onboarding), but also allows firms to scale their activities significantly without ceilings resulting from inefficient processes. Automation in investment management also fuelled the massive shift towards passive investments over the past two decades, and more recently robo-advisors / systematic

Legal Contract Standardisation and RegTech

This driver results in significantly reduced overheads to draft, negotiate, and confirm legal and marketing documents. In the cases of financial contracts, it minimizes the risk of legal or regulatory misalignment with a trade’s economics. See this article by EY that expands on the topic.

Vertical Integration

Properly structured data that flows seamlessly across an entire organization eliminates duplicate / incompatible data or systems and the necessity for bespoke or human interfaces. Vertical integration also provides significant improvement of management, finance, and compliance oversight as all activities can be monitored versus a firm’s Key Performance Indicators. For a deeper dive into the topic, see here.

Artificial Intelligence

This technology mimics human problem-solving and decision-making processes allowing financial services firms to operate more efficiently, reduce fraud, explore new revenue streams, and interrogate the rich data sets hidden in their databases and the economy at large. Robotic process automation will eliminate low-grade tasks, enabling humans to focus on higher value activities. The more data consumed by AI-powered tools, the better the results, so the data-rich financial markets and customers stand to massively benefit.

Blockchain Technology & Smart Contracts

This is a game-changer for the entire industry. Disintermediation makes costly, complex, manual and rent-seeking behavior obsolete and leads to a faster, more efficient, transparent, and correct market infrastructure. This massive value released goes towards cost savings in financial services firms and, most importantly, makes finance more affordable and accessible, improving investors’ real returns. It should be clear that this technology is not just disruptive, yet foundational, a view well articulated by Harvard Business Review. Another far-reaching implication of blockchain that cannot be stressed enough is decentralized identities – if you are unfamiliar with this concept check out these two articles by HBS and Microsoft Identity Division.

Cloud Technology

Storing data on the cloud empowers financial services firms with rapid deployment of computing resources that scale efficiently according to business needs and growth. There already exist options that are secure and compliant with all existing regulations. It is no surprise that Credit Suisse Co-CIO called this direction inevitable and most major financial institutions, like the World Bank and Capital One, are already migrating to cloud-based data storage.

Open Architecture, Open Banking Standards, and Access Protocol Interfaces (API)

The recent Payment Services Directive (PSD2) (known as “Open Banking”) forces financial services firms to make customer data available between authorized organizations online in order to foster innovation and bolster competition — Seventy-seven per cent of global banks will have invested in Open Banking by 2019. This Wired article explains more here. Additionally, firms have been transforming their IT systems to an “open architecture” approach providing secure access via APIs to a wide range of other institutional services outside their firms to strengthen customer retention.

Open Source Software

Nowadays it rarely makes sense for a firm to develop every piece of needed software. There is a proliferation of production-grade open source enterprise software being maintained by legions of engineers and developers worldwide. A recent proof of this tectonic shift is IBM, a major provider of services to financial firms, recently announced its largest acquisition ever, the purchase of Linux for $34 billion. See here for an interesting article on open source driving innovation.

Regulatory Landscape

One must not undermine the wide-reaching responses to the previous financial crisis from regulators promoting transparency, innovation, and competition across the global financial system.

The introduction of the General Data Protection Regulation (GDPR) and Markets in Financial Instruments Directive (MiFID II), leads to increased product and service transparency for investment solutions.

Quantum Computing

Quantum computing represents such transformational opportunity that it is almost inconceivable to most. To illustrate, as of 2015, Google created a quantum computer that is…wait for it… 100 million times faster than anything on the market today. The implications for finance are endless such as algorithmic enhancement and improved risk modeling. The possibilities have even given birth to a whole new discipline called Quantum Finance.

Mobile-First

Banking 4.0 starts in our pockets. Migrating platforms and optionality on our fingertips provides clients and investors with more real-time decision making and information when they are away from their desks. And to show just how ready the world is for increased usage, Oracle recently stated that sixty-seven percent of customers globally are on digital banking platforms now with the World Bank reporting that in the last three years alone, 515 million customers worldwide opened a banking account through a mobile money provider. A complete list of mobile banking penetration by country can be found here.

Social Media

The wisdom of the crowds has never been so transparent in the age of information and thus never been so powerful in our ability to comprehend markets but also move them. Like many other technologies in financial services, however, the insights from the chatter have been on a delayed cycle compared to other industries and applications. A report from GNIP suggests that social media analytics is just reaching “the exciting inflection points where costs and barriers to use have decreased, allowing new entrants the ability to gain an information advantage”.

Internet of Things (IoT)

At first glance, IoT application in capital markets is difficult to picture until you realize that the lifeblood of these markets is data. IoT provides edge-case and near real-time acquisition points of alternative data that feeds into the holistic picture of a business. One of the most tangible use-cases is the application in commodities trading, where sensors give a plethora of data about source conditions allowing market participants to better forecast yields. Some of the less apparent use cases of IoT in financial services include insurance (e.g. micro-sensors giving fair insurance premia), but go as far as security, monitoring, and customer experience.

Drivers of Change in Capital Markets

A New Emerging Ecosystem

The emerging picture is an ecosystem of small and agile Fintech companies, whose unique capabilities will be tapped by the larger capital markets players to provide enhanced insights, products, and services to their global clientele. The challenge, however, for established players is to stay on top of these developments and to make sense of how this ecosystem evolves, in order to steer their organizations safely toward the future and not fall prey to Gartner’s 2018 CEO survey predictions. Change itself is now a consistent and dynamic driver and some of the aforementioned technologies and trends will be part of the convergence that transforms the financial services landscape for decades to come.

Next week’s article will focus on one technological driver which is arguably the most impactful, blockchain technology. Blockchain will be a game-changer for the entire financial services industry and a way to remove layers of intermediaries making markets more transparent, efficient and accessible – among a variety of other important aspects. The number and gravitas of financial services firms investing both time and money into blockchain technology is a testimony to the growing trend and evidence that this is only the beginning. Stay tuned!

In this series of articles, I cover the current challenges, the applicable technologies, and how some Fintech companies are harnessing the inevitable tides of change. Please share your comments and feedback as I explore these topics – from seasoned professionals, to technologists, to the eternally curious!

The author, Hariton Korizis, is the co-founder of ResonanceX along with Guillaume Chatain. The company is participating in the Barclays Techstars NYC Accelerator, the Kickstart Accelerator in Zurich, the UK Investment Association’s Velocity Accelerator in London, and is regulated by the UK’s Financial Conduct Authority. In March 2018 the world’s first Structured Product to be cleared and settled on the open public Ethereum blockchain was issued through the ResonanceX platform. The transaction was automated end-to-end, and fully compliant with existing laws and regulations, setting the foundation for how Structured Products can be traded from now into the future.

#ResonanceXseries #CapitalMarkets #Innovation #StructuredInvestments